※ The following instructions and terms are subject to Chinese exposure

以下相關說明與條款皆以中文揭露為準

※ All dollar amounts below are denominated in NTD / January 2026 Edition

金額表示皆以新臺幣計/115.01修訂版

CTBC Credit Card User Guide

中國信託商業銀行信用卡用卡須知

Late Fee 逾期還款違約金

1.Cardholders will incur a late fee if they do not pay the minimum payment due on or before the payment due date (i.e. late payment). Late fee is calculated in the following manner: A late fee of NT$300 will be charged if payment is late for one billing cycle. A late fee of NT$400 will be charged if payment is late for 2 billing cycles. A late fee of NT$500 will be charged if payment is late for 3 billing cycles. A cardholder will not incur a late fee if the unpaid balance in his/her monthly statement (balance due for the current billing cycle minus annual fee, finance charges, late fee, other charges (including but not limited to cash advance fee, card loss report fee, sales draft retrieval fee, copy statement fee or foreign transaction service fee) and unpaid amount by the cardholder up to the payment due date for the current billing cycle) is less than NT$1,000. If a cardholder has late payment for three consecutive cycles or more, the cardholder will be charged a late fee up to three times. 2. Whether a dual-currency cardholder is deemed to have late payment and incur a late fee will be determined by the total NTD payment made by the cardholder (the sum of payment made in the agreed foreign currency converted into NTD based on CTBC exchange date on the payment due date plus payment made in NTD); if the total NTD payment made is less than the minimum payment due, the cardholder is deemed to have a late payment and must pay a late fee. Example: (An example of USD-NTD dual-currency card) the customer's billing statement shows NT$10,000 balance due and $1,000 minimum payment due; US$300 balance due and US$30 minimum payment due. On the payment due date, the customer pays NT$1,000 and deducts automatically US$30 from his USD account. His total payment is then NT$1,900 based on CTBC's exchange rate on the payment due date ($1,000 + US$30 x exchange rate 30 = $1,900). How to determine whether the customer has paid enough minimum payment: By comparing the total payment made in NTD $1,900 with the sum of NTD equivalent of minimum payment due ($1,000 + US$30 x exchange rate 30 = $1,900), the customer is not required to pay a late fee. 3. Calculation (using the example on finance charges above): If Mr. A did not to pay the minimum payment due on or before 4/23, the payment due date for the 4/5 statement, the 5/5 statement will show a late fee of NT$300; if Mr. A still did not pay the minimum payment due before 5/23, which means Mr. A is late for 2 billing cycles, the 6/5 statement will show an additional late fee of NT$400.

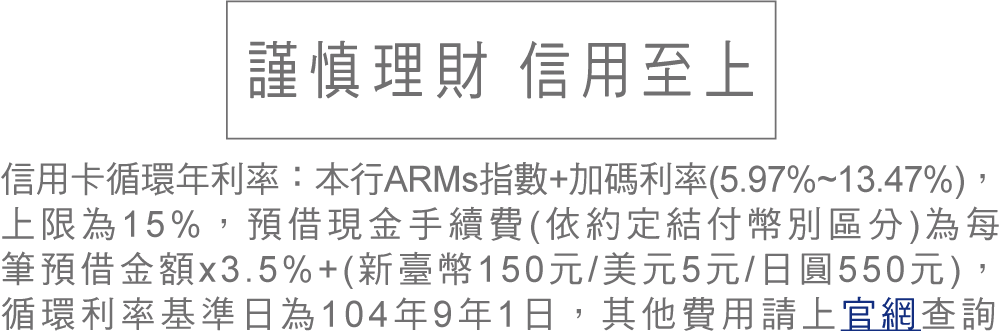

1.持卡人如未於繳款截止日前繳足最低應繳金額時(即逾期繳款),應以下列方式計付違約金(即逾期還款違約金):逾期繳款達1期者,應繳交違約金新臺幣(下同)300元。逾期繳款達2期者,應繳交違約金400元。逾期繳款達3期者,應繳交違約金500元。如持卡人每月帳單未繳清金額(以當期之應付帳款扣除年費、循環信用利息、違約金、各項應繳手續費(包括但不限於預借現金手續費、掛失停用手續費、違約金、調閱簽帳單手續費、補寄帳單手續費或國外交易手續費)及持卡人至當期繳款截止日止已繳付之帳款後之未繳清金額)在新臺幣1,000元(含)以下者,無須繳納違約金;持卡人發生前項應計付違約金之情事達連續三期以上(含)者,其應付之違約金,則以三期為上限。2.雙幣卡帳款是否遲繳,而須繳納違約金,將依持卡人歸戶新臺幣總繳款金額(即依繳款截止日當天本行匯率,將約定外幣總繳款金額轉換為約當新臺幣金額後,加計新臺幣總繳款金額後之總和)判斷;若未繳足歸戶新臺幣總繳款金額之最低應繳款金額,則視為延遲,需繳納違約金。計算範例說明:(以美元雙幣卡為例)客戶本期帳單上之新臺幣應繳總金額新臺幣10,000元,最低應繳款新臺幣1,000元;美元應繳總金額美元$300元,美元最低應繳款美元$30元。繳款截止日時客戶以臺幣繳款新臺幣1,000元,美元帳戶自動扣款美元$30元,則依繳款截止日當天本行匯率換算客戶歸戶總繳款金額約當新臺幣1,900元(1,000+美元繳款30×匯率30=1,900元)是否繳足最低應繳款之判斷:以歸戶新臺幣總繳款金額新臺幣1,900元與約當新臺幣最低應繳款總和(新臺幣)=1,000+美元最低應繳款30×匯率30=1,900元判斷,客戶有繳足最低應繳款,故客戶不需繳交違約金。3.計算說明(承上循環信用利息案例):若某甲於4月23日繳款截止日前未繳付最低應繳款,則於5月5日帳單結帳時,另需繳納逾期還款違約金新臺幣300元;又於5月23日繳款截止日前仍未繳付最低應繳款,致逾期繳款達2期,則6月5日帳單結帳時,另需繳納逾期還款違約金新臺幣400元。

Authorized Exchange Settlement for Foreign Transactions 國外交易授權結匯

All credit card transactions shall be paid in NTD or the agreed foreign currency. When the currency of transaction (including refunds) is other than NTD, the cardholder authorizes CTBC to convert the transaction amount into NTD or the agreed settlement currency based on the exchange rate provided by the international credit card organizations on the date of exchange settlement and add the fees that CTBC must pay international organizations as well as a foreign transaction service fee charged by CTBC at 0.5% of the transaction amount; no foreign transaction service fee will be charged in case of refunds. (Fees charged by international credit card organizations will be determined by such organizations. Please visit CTBC website for details) Unless it is otherwise agreed, all transactions (including refunds) that incur added fees as described above will be settled in NTD, including NTD transactions charged abroad and NTD transactions charged in Taiwan where merchant's acquiring bank is a foreign bank (including online transactions). The exchange rate applicable to refunds may differ from that used for the purchase transaction due to the time of exchange settlement, which means the cardholder may incur exchange loss. The cardholder authorizes CTBC to be his or her exchange settlement agent in the Republic of China to handle the exchange settlement formalities for his or her foreign-currency credit card transactions taken place abroad. However if the amount of exchange settlement payable by the cardholder exceeds the regulatory limit, the cardholder shall pay the amount exceeding the regulatory limit in a foreign currency.

持卡人所有使用信用卡交易帳款均應以新臺幣或約定外幣結付,如交易(含辦理退款)之貨幣非為新臺幣時,則授權發卡機構依各信用卡國際組織依約所列之結匯日匯率直接換算為新臺幣或約定結付外幣,加計發卡機構應向各該國際組織給付之手續費,及發卡機構以交易金額之0.5%計算之國外交易服務費後結付;如為退款,則不加收國外交易手續費。(各信用卡國際組織收取費率係依該組織規定,詳見本行網站說明)除另有約定外,加計前述費用之交易(含辦理退款)係以新臺幣結付,且包含國外刷卡之新臺幣交易,以及國內刷卡但商店的收單銀行為外國銀行之新臺幣交易(含網路交易)。退款適用之匯率可能因結匯時間不同,而與其交易時適用之匯率不同,可能產生匯兌損失。持卡人授權發卡機構為其在於中華民國境內之結匯代理人,辦理信用卡在國外使用信用卡交易之結匯手續,但持卡人應支付之外幣結匯金額超過法定限額者,持卡人應以外幣支付該超過法定限額之款項。

Card Loss Report Fee 掛失停用手續費

CTBC charges NT$100 per card reported loss (1. No such fee for Infinite Card/ World Card /Eternity Card; 2. Taipei 101 cardholders are eligible for one exemption of Taipei 101 card loss report fee each year).

每卡100元(1.鼎極卡不收取。2.TAIPEI 101持卡人每年可享1次TAIPEI 101卡免收掛失費100元。)

Sales Draft Retrieval Fee 調閱簽單手續費

CTBC charges NT$50 per transaction, domestic or foreign (no such fee for Infinite Card/ World Card /Eternity Card and transactions not authorized by the cardholder).

不分國內國外消費每筆50元(鼎極卡、非持卡人本人交易不收取)

Copy Statement Fee 補寄帳單手續費

CTBC charges NT$100 per statement for past credit card statements that are three months or older.Except for finance charges and interest rate, CTBC may adjust credit card fees and charges and late fee once every year starting May 1, 2010. But if any charges or late fee is lowered or canceled, CTBC may make such adjustment at any time.

補發3個月以前帳單,每月份補發手續費100元。本行信用卡各項費用、循環信用利率、循環信用利息及違約金之調整頻率,除循環信用利率、循環信用利息外,自民國99年5月1日起,本行每年得調整一次;如有費用、違約金收取金額調降或取消收取,本行得隨時調整。

Express Delivery Charges快遞服務費

NT$150 per card (payment due only when it is stated in the billing statement).

每卡150元(待帳單通知時,才須繳費)

Loss of Card and Other Situations 卡片遺失等情形

1.If the cardholder’s credit card is lost, stolen, robbed, lost in a swindle, or taken possession by another person other than the cardholder (collectively referred to as“lost”), the cardholder should promptly notify CTBC or CTBC-designated establishments by phone or by other means to report the card loss and pay a card loss report fee of NT$100. If deemed necessary by CTBC, a notice will be sent to the cardholder within 10 days after accepting the card loss report, requesting the cardholder to file a report with the local police authority within 3 days after receiving the notice or send a written supplementary report to CTBC. 2.CTBC will assume losses incurred from unauthorized use of the cardholder’s credit card starting from the time the cardholder has completed the card loss report formality. However, under any of the following circumstances, the cardholder shall still be held liable for losses incurred from unauthorized use after completing the card loss report formality: (1)The unauthorized use by another individual is permitted by the cardholder or the cardholder intentionally gave his or her card to said individual. (2)Another individual learns the cardholder’s password or other ways to verify the identity of the cardholder for cash advances or other transactions via ATM as a result of an intentional act or material omission on the part of cardholder. (3)The cardholder conspired with a third party or merchant to falsify transactions or to commit credit card fraud. 3.The amount (deductible) to which the cardholder is liable for losses incurred from unauthorized credit card use prior to completing the card loss report formality shall be capped at NT$3,000. However, the cardholder’s deductible may be waived under any of the following circumstances: (1)Unauthorized card use occurred within 24 hours before the completion of the card loss report formality; or (2)The signature of the unauthorized user on the sales draft appears visibly different to the naked eye from the signature of the cardholder, or identifiably different from the signature of the cardholder had due diligence of a good administrator been exercised. 4.If the cardholder has a situation specified in the proviso of Paragraph 2 hereof and one of the following conditions, and CTBC could show that it has exercised due diligence of a good administrator, the agreed deductible for unauthorized use in the preceding paragraph does not apply: (1)The cardholder is aware that his or her credit card has been lost or stolen, but is remiss in promptly notifying CTBC, or if the cardholder still did not notify CTBC of lost or stolen credit card 20 days after the current payment due date. (2)The cardholder did not sign on his or her credit card immediately after receiving the card, which results in unauthorized use by another individual. (3)The cardholder did not provide the documents requested by CTBC, refused to assist with the investigation or show other behaviors that violate the principle of good faith after reporting credit card loss. 5.Regarding cash advances at ATM, the cardholder shall be liable for losses resulting from fraudulent use of his/her credit card occurred prior to reporting of the card loss and the deductible specified in Paragraph 3 does not apply.

1.持卡人之信用卡如有遺失、被竊、被搶、詐取或其他遭持卡人以外之他人占有之情形(以下簡稱遺失等情形),應儘速以電話或其他方式通知本行或其他經本行指定機構辦理掛失手續,並繳交掛失手續費每卡新臺幣100元。但如本行認有必要時,應於受理掛失手續日起十日內通知持卡人,要求於受通知日起三日內向當地警察機關報案或以書面補行通知本行。2.持卡人自辦理掛失手續時起被冒用所發生之損失,概由本行負擔。但有下列情形之一者,持卡人仍應負擔辦理掛失手續後被冒用之損失:(1)他人之冒用為持卡人容許或故意將信用卡交其使用者。(2)持卡人因故意或重大過失將使用自動化設備辦理預借現金或進行其他交易之交易密碼或其他辨識持卡人同一性之方式使他人知悉者。(3)持卡人與他人或特約商店為虛偽不實交易或共謀詐欺者。3.辦理掛失手續前持卡人被冒用之自負額以新臺幣3,000元為上限。但有下列情形之一者,持卡人免負擔自負額:(1)持卡人於辦理信用卡掛失手續時起前二十四小時內被冒用者。(2)冒用者在簽單上之簽名,以肉眼即可辨識與持卡人之簽名顯不相同或以善良管理人之注意而可辨識與持卡人之簽名不相同者。4.持卡人有本條第二項但書及下列情形之一,且本行能證明已盡善良管理人之注意義務者,其被冒用之自負額不適用前項約定:(1)持卡人得知信用卡遺失或被竊等情形而怠於立即通知本行,或持卡人發生信用卡遺失或被竊等情形後,自當期繳款截止日起已逾二十日仍未通知本行者。(2)持卡人於收到信用卡後,未立即於信用卡簽名致他人冒用者。(3)持卡人於辦理信用卡掛失手續後,未提出本行所請求之文件、拒絕協助調查或有其他違反誠信原則之行為者。5.在自動化設備辦理預借現金部分,持卡人辦理掛失手續前之冒用損失,由持卡人負擔,不適用第三項自負額之約定。

Procedure for Handling Questionable Card Charges 帳款疑義之處理程序

1.When the cardholder and a merchant or a commissioned cash advance provider have dispute over the quality, quantity, or dollar amount of product or service purchased, or the dollar amount of cash advance received, the cardholder should resolve the dispute with the merchant or the commissioned cash advance provider, and may not use it as an excuse for not paying CTBC balance due. 2.When the cardholder runs into any of the following extraordinary circumstances in the use of credit card as provided by the credit card organization, for instance, the ordered product was not delivered by the merchant or the quantity did not match, the ordered service was not provided, or no money was received in a cash advance via ATM or the amount of cash obtained was incorrect, the cardholder should first resolve the issue with the merchant or the cash advance provider. 3.If the cardholder has any question concerning any transactions stated in the billing statement, the cardholder may, before the payment due date, notify CTBC for assistance by providing reasons and support documents requested by CTBC (e.g. sales draft or refund slip), or by agreeing to pay for a sales draft retrieval fee of NT$50 per draft to obtain a copy of the sales draft or the refund slip from the acquirer. For cardholders who ask CTBC to request a copy of the sales draft or refund slip from the acquirer by paying a service fee, once the result of the investigation indicates that the cardholder has fallen victim to unauthorized uses of credit card or that the questionable charges cannot be attributed to the fault of the cardholder, CTBC will be responsible for the retrieval fee. 4.If the cardholder intends to withhold payment, the cardholder may ask CTBC to request chargeback from the acquirer or the cash advance provider, or request arbitration by the international credit card organization or make other requests after paying a processing fee determined by the international credit card organization for handling dispute and may request CTBC to withhold payment regarding the particular transaction. 5.For disputed charges on which payment is withheld, if the cardholder disagrees to pay the aforementioned processing fee or if CTBC later finds that the charge is not erroneous or that payment should not be withheld for the dispute is not caused by something attributable to the fault of CTBC, the cardholder shall make payment immediately upon receiving a notice from CTBC, and pay CTBC interest at then applicable rate on finance charges (15% APR at maximum) starting from the next day following the original payment due date. 6.When a dispute occurs between the cardholder and a merchant, CTBC will provide assistance in resolving such dispute and be an advocate for the consumer when there are any doubts.

1.持卡人如與特約商店就有關商品或服務之品質、數量、金額,或與委託辦理預借現金機構就取得金錢之金額有所爭議時,應向特約商店或委託辦理預借現金機構尋求解決,不得以此作為向本行拒繳應付帳款之抗辯。2.持卡人使用信用卡時,如符合各信用卡組織作業規定之下列特殊情形:如預訂商品未獲特約商店移轉商品或其數量不符、預訂服務未獲提供,或於自動化設備上預借現金而未取得金錢或數量不符時,應先向特約商店或辦理預借現金機構尋求解決。3.持卡人於當期繳款截止日前,如對帳單所載之交易明細有疑義,得檢具理由及本行要求之證明文件(如簽帳單或退款單收執聯等)通知本行協助處理,或同意負擔調單手續費每筆新臺幣50元整後,請本行向收單機構調閱簽帳單或退款單。持卡人請求本行向收單機構調閱簽帳單或退款單時,約定由持卡人給付調單手續費者,如調查結果發現持卡人確係遭人盜刷或帳款疑義非可歸責於持卡人之事由時,其調單手續費由本行負擔。4.如持卡人主張暫停支付時,於其同意依各信用卡國際組織作業規定繳付帳款疑義處理費用後,得請本行向收單機構或辦理預借現金機構進行扣款、信用卡國際組織仲裁等主張,並得就該筆交易對本行提出暫停付款之要求。5.因發生疑義而暫停付款之帳款,如持卡人不同意繳付前項帳款疑義處理費用或經本行證明無誤或因非可歸責於本行之事由而不得扣款時,持卡人於受本行通知後應立即繳付之,並自原繳款期限之次日起,依持卡人當期適用之循環信用利率(最高年息為15%)計付利息予本行。6.持卡人與特約商店發生消費糾紛時,本行應予協助,有疑義時,並應為有利於消費者之處理。

Credit Limit 信用額度

CTBC will grant a credit limit to the cardholder in view of his or her credit status. After the grant, CTBC may adjust the credit limit upon the request of cardholder or after obtaining the written consent of cardholder or according to the procedure approved by the competent authority, and notify the cardholder of the adjustment. When a cardholder applies for a second credit card from CTBC (including supplementary card), the applicant should provide other proofs of financial capacity and CTBC will increase the cardholder's credit limit after obtaining cardholder's written consent. A cardholder and his/her supplementary cardholders will share the same credit limit granted by CTBC, regardless of the number and types of CTBC credit cards the cardholder has, and should not charge their cards over that credit limit. A dual-currency card and other credit cards issued by CTBC to the same cardholder also share the same credit limit that the available credit for charges in NTD and the agreed foreign currency will be combined into the total available credit under cardholder's NTD account at CTBC. CTBC will carry out risk management based on the total credit limit granted to cardholder's NTD account.

本行得視持卡人之信用狀況核給信用額度,核給後得依持卡人自行申請、或取得持卡人書面同意、或依其他主管機關核可之程序調整其信用額度,並通知持卡人。凡已持有本行信用卡,再申請本行第二張以上信用卡時(含附卡),請檢附其它財力證明,本行將於持卡人書面同意後酌予提高信用額度。持卡人(含附卡持卡人)無論持用本行信用卡張數、種類,均共用同一之信用額度,不得超過該信用額度使用信用卡。雙幣卡與其他信用卡共用同一信用額度,新臺幣與約定外幣整體可使用之信用額度合併於持卡人於本行新臺幣歸戶可使用總額度。本行將就持卡人新臺幣歸戶總額度進行風險控管。

Important Notes for Student Cardholders 學生使用信用卡應行注意事項

1.Before you start using CTBC credit card, please carefully read the agreement we send you to understand the rights and obligations of both parties. 2. For non-student applicants age 18~24, CTBC will inquire whether the applicant is a student. If this is the case, CTBC will process the application as a student application and apply all rules on student cardholders. 3. Before CTBC issues a credit card to a student applicant, CTBC will notify the applicant's parent(s) of card issuance as required. If so requested by a student cardholder's parent(s) (or legal guardian), CTBC may adjust cardholder's credit limit or suspend cardholder's card use privileges. In such case, Article 23 of the Credit Card Agreement applies. CTBC will reinstate the student cardholder's card use privileges after the cardholder provides a "Confirmation of Parental Consent to Reinstatement of Credit Card" and proof of financial capacity.

1.在您使用中國信託信用卡前,請詳閱本行寄送之約定條款,以充分了解雙方之權利義務。2.對於十八至二十四歲之非學生身份申請人,本行將依規主動瞭解並查詢其是否具有學生身份,若經本行查證申請人確有學生身份時,將逕依本行學生持卡人發卡流程處理之,並即適用本行有關學生持卡人之所有規範。3.學生申請人若獲本行發卡時,本行將依規函知學生父母發卡情事;本行亦得因學生父母(或監護人)要求,不經事先通知而調整持卡人之信用額度或暫時停止其使用卡片之權利,並準用「信用卡約定條款」第二十三條之規定辦理。本行得於持卡人提出「父母同意恢復用卡確認書」及財力證明後,恢復持卡人使用信用卡之權利。

Outsourcing 本行委外處理

The applicant agrees that if deemed necessary, CTBC may commission suitable third parties or cooperate with member institutions of the credit card organizations to handle the billing and payment operations, computer processing operation or other credit card related operations (e.g. information system data entry, processing and output, information system development, monitoring and maintenance, marketing, customer data input, form printing, packing and delivery/mailing, safekeeping of forms, certificates and other documents, card production and delivery, payment collection and legal proceedings, etc.【including collection, computer processing, international transmission and use of personal data that meet specific purposes】) that may be outsourced in accordance with the regulations set forth by the Financial Supervisory Commission or as approved by the Financial Supervisory Commission and provide the applicant's personal data to such third parties for the aforementioned purposes.

申請人同意本行,就交易帳款收付業務、電腦處理業務或其他與信用卡有關之附隨業務(如資訊系統之資料登錄、處理及輸出,資訊系統之開發、監控及維護,行銷,客戶資料輸入,表單列印、裝封及付交郵寄,表單、憑證等資料保存,卡片製作及送達,帳款催收及法律程序,等【含符合特定目的之相關個人資料蒐集、電腦處理、國際傳遞及利用】),於必要時得依金融監督管理委員會規定或經金融監督管理委員會核准,委託適當之第三人或與各信用卡組織之會員機構合作辦理,並依前述目的將個人各項資料提供予該第三人。